GR MITCHELL’S COVID-19 RESPONSE

March 16, 2020

THE BEST TIME OF YEAR TO REPLACE WINDOWS

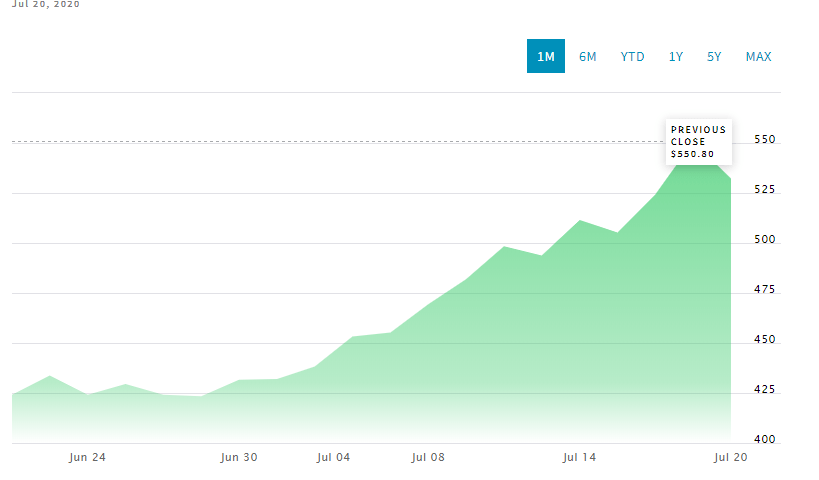

September 1, 2020LUMBER MARKET UPDATE – JULY 2020

Costs of your projects skyrocketing? Finding it harder to find the materials you need?

Well, you’re not alone. It’s fairly common for a commodity good, like lumber, to experience price and availability fluctuations. But recent changes in the lumber market are likelymore drastic than you’ve ever seen before and it’s creating challenges for DIY’ers, remodelers, and builders across the board (not to mention suppliers, like GR Mitchell).

Well, you’re not alone. It’s fairly common for a commodity good, like lumber, to experience price and availability fluctuations. But recent changes in the lumber market are likelymore drastic than you’ve ever seen before and it’s creating challenges for DIY’ers, remodelers, and builders across the board (not to mention suppliers, like GR Mitchell).

The Problem

in late March the potential severity of COVID became a grave concern to local governments causing construction to slow nationwide while in some states, like Pennsylvania, it came to a screeching halt. The sudden drop in demand sent prices plummeting to their lowest rate since February of 2016. Fast forward to today; Prices have more than doubled since.

The current status of the market can be easily summarized – lumber is harder to find and more expensive as a result.

As COVID emerged as a threat to the western world, stay at home orders shut down some mills entirely for months, while others continued to operate under reduced capacity as a result of social distancing guidelines. As safer working procedures became clearer mills were intentionally slow to react in anticipation of a major slump in demand driven by adverse effects on the housing industry. But that assumption would prove to be wildly inaccurate.

The current status of the market can be easily summarized – lumber is harder to find and more expensive as a result.

So, What Happened to the Supply?

Prior to COVID entering the picture lumber mills had already made the decision to curtail production. This was in an effort to combat unfavorable stumpage rates and sustained lower pricing, manipulating the market to reduce supply was a path to ultimately increase their profits.As COVID emerged as a threat to the western world, stay at home orders shut down some mills entirely for months, while others continued to operate under reduced capacity as a result of social distancing guidelines. As safer working procedures became clearer mills were intentionally slow to react in anticipation of a major slump in demand driven by adverse effects on the housing industry. But that assumption would prove to be wildly inaccurate.

Despite challenges from the virus including elevated unemployment rate, the housing market rebounded sooner and with faster velocity than they had anticipated. With housing starts increasing 17.3% in June alone (according to the NAHB), low mortgage rates combined with the continuation of the pre-existing housing shortage and brand-new demand in lower density markets (think small metro areas and exurbs) the lumber need quickly became out of balance with the supply.

But new homes aren’t the only unexpected drain on the already lean inventory, the uptick in DIY demand was also unanticipated. With time on their hands and budgets freed up by canceled summer travel plans, consumer strain on the supply chain hit unseen levels, too.

Bottom line – construction demand surpassed mills’ projections.

But new homes aren’t the only unexpected drain on the already lean inventory, the uptick in DIY demand was also unanticipated. With time on their hands and budgets freed up by canceled summer travel plans, consumer strain on the supply chain hit unseen levels, too.

Bottom line – construction demand surpassed mills’ projections.

Big Concerns & Market Variables

Weather. Wildfires. Railcar availability. Factors that we commonly are concerned about as summer comes to a close. It’s radically clear though, you’d be hard pressed to describe 2020 as common. New variables are in play concurrent with typical seasonal anxieties.

2×4’s and 2×6’s are particularly volatile causing new home builders specifically to feel the pinch.Entry-level and mid-range homes account for a growing segment of the new home market (projects with lower dollar profitability than high-end counterparts). With framing lumber accounting for roughly 1/5th of the material cost, the rise in lumber prices leaves little room for error in already tight financial plans. To keep housing prices in an affordable range and to retain profit on existing contracts changes will likely be in order; Do you sacrifice on finishes? Do you reduce the size of homes (the 2018 spike commonly lead to reduction of sq footage)? Do you build further into suburban/rural areas with lower land cost? That’s yet to be seen.

Treated lumber, a pain point for many in recent months, continues to suffer from supply chain issues as well. Outdoor projects lead the charge for many this summer. While increased demand this time of year is common, elevated homeowner projects were matched by restaurants and bars seeking creative solutions to indoor seating restrictions. Construction of new decks became a business-saving measure for many, seeing outdoor seating as their only viable way to keep their doors open. Chemical treatment facilities are likely to be the next bottleneck in treated production for some geographies as orders continue to be almost double of this time last year.

Undoubtedly politics has played a factor in almost every step of COVID response and as the nation navigates a turbulent presidential election the lumber industry is likely to feel the impact of politics further. Tariffs have been a hot button issue in the past year and imports from Canada (including a wide variety of forestry goods) are no different. In the current market, such tariffs continue to cause elevated prices. The election could also set the stage for a (much needed) focus on nationwide infrastructure improvements. Updates to bridges, airports, etc have the potential to keep demand higher than normal.

So, how should you proceed? Based on our observations you might be best served in waiting to purchase, if possible. And, in some cases, you may have to wait as the volume you need may not be immediately available. The longer you can hold out on making larger purchases, the better. In scenarios in which you need to estimate projects entering construction late summer/early fall, be overly cautious and leave some room for the lumber market to make further unprecedented price shifts in the short-term.

Undoubtedly politics has played a factor in almost every step of COVID response and as the nation navigates a turbulent presidential election the lumber industry is likely to feel the impact of politics further. Tariffs have been a hot button issue in the past year and imports from Canada (including a wide variety of forestry goods) are no different. In the current market, such tariffs continue to cause elevated prices. The election could also set the stage for a (much needed) focus on nationwide infrastructure improvements. Updates to bridges, airports, etc have the potential to keep demand higher than normal.

Plan Your Purchases

With mills returning to full production capacity, there’s a push to catch-up to demand, but it’s unlikely that relief will be felt until late fall. Historically long lead times continue to push lumber futures up with the fear that they could eclipse the 2018 record peak. And with no shortage of variables and unknowns impacting the market, many in the industry are left stabbing in the dark when trying to anticipate what’s coming next. GR Mitchell is fortunate to have boots-on-the-ground; AKA long tenured, in-house purchasers focused solely on buying for a single, local yard. And while inventory availability is still a looming threat for some items in Willow Street, purchasing agility has helped to keep volatility low when compared to many other suppliers.So, how should you proceed? Based on our observations you might be best served in waiting to purchase, if possible. And, in some cases, you may have to wait as the volume you need may not be immediately available. The longer you can hold out on making larger purchases, the better. In scenarios in which you need to estimate projects entering construction late summer/early fall, be overly cautious and leave some room for the lumber market to make further unprecedented price shifts in the short-term.